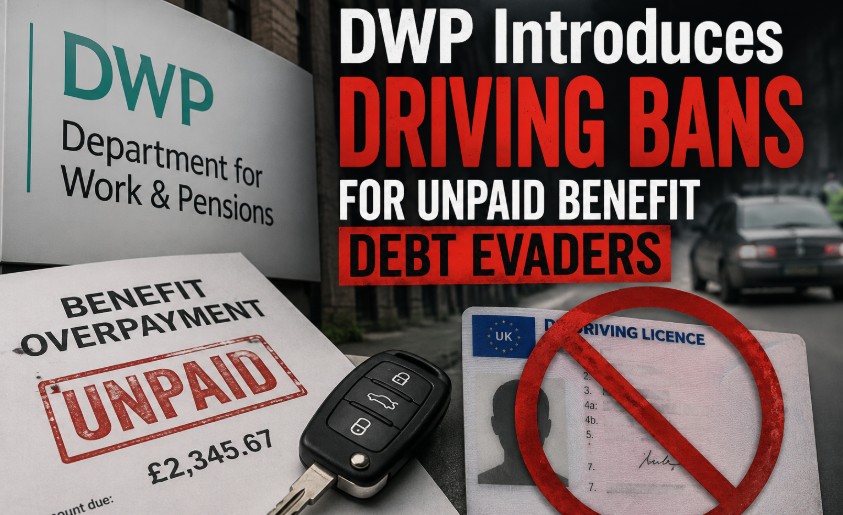

The Department for Work and Pensions (DWP) can now apply for court-ordered driving bans and execute direct bank account deductions to recover outstanding welfare overpayments from individuals who intentionally avoid repayment.

Under the Public Authorities (Fraud, Error and Recovery) Act 2025 (PAFER Act), these enforcement mechanisms specifically target former claimants who are out of the PAYE and active benefit systems.

Warning letters are being distributed as of June 2026, establishing a strict four-month administrative window before formal enforcement phases begin in October 2026.

What Are the New DWP Debt Recovery Powers Under the PAFER Act 2025?

As of June 2026, the Department for Work and Pensions has activated enhanced legal mechanisms via the Public Authorities (Fraud, Error and Recovery) Act 2025, widely known as the PAFER Act.

According to the National Audit Office (NAO), this structural legislative overhaul grants administrative bodies unprecedented recovery options to reclaim a projected £14.6 billion over five years from welfare fraud, claimant errors, and unaddressed overpayments.

Closing the Out-of-System Loophole for Former Claimants

The DWP is closing the out-of-system loophole by isolating former claimants who possess the financial capacity to pay debts but choose to evade contact, specifically targeting individuals operating outside standard PAYE employment or active benefit deduction systems.

The new legislative framework directly closes this loophole. When reviewing debt collection profiles, the DWP intends to deploy these punitive measures as an escalation strategy rather than a first-line response.

The focus remains tightly fixed on systemic debt evasion rather than active benefit recipients whose deductions are already managed via automated statutory limits.

Why Does DWP Introduce Driving Bans for Unpaid Benefit Debt Evaders?

The DWP introduces driving bans for unpaid benefit debt evaders to act as a powerful non-financial compliance lever. The ban targets social and lifestyle convenience, forcing willful non-compliers who hide assets or avoid PAYE tracking to re-engage with debt management services.

The driving ban mechanism under the PAFER Act 2025 is a targeted enforcement tool designed to address specific systemic gaps:

- Targets Willful Non-Compliers: Forces individuals who have left the welfare and PAYE systems—but possess the financial means to pay, to engage with the DWP rather than ignoring communication.

- Acts as a Non-Financial Incentive: While bank deductions target hidden funds, a driving ban threatens personal convenience. Because the ban is instantly suspended once a repayment plan is agreed upon, it functions as a lever for compliance rather than just a punishment.

- Protects Public Funds: Aims to recover part of a projected £14.6 billion loss from welfare fraud and errors, signaling that public debt cannot be outwaited.

- Isolates Social Convenience: By exempting those who rely on driving for their livelihood or caregiving, the law strictly penalizes those who choose lifestyle convenience over legal debt obligations.

When Do the New DWP Driving Bans and Bank Deductions Take Effect?

The new DWP driving bans and bank deductions take effect across a dual-phase timeline: statutory warning letters commenced on 24 June 2026, establishing a four-month grace window before full enforcement and court applications begin in October 2026.

The Enforcement Timeline (June 2026 – October 2026)

The execution schedule operates across strict operational milestones:

- 24 June 2026 (Statutory Commencement): The DWP officially initiated the mailing of updated, statutory debt warning notices to thousands of individuals with unaddressed overpayment balances. These letters serve as formal legal notifications.

- The Four-Month Grace Window: Recipients are granted exactly four months from the receipt of the initial warning letter to contact standard DWP debt management services. Engaging within this timeframe to establish an affordable installment plan completely halts any escalation toward bank clawbacks or licence suspensions.

- October 2026 (Full Enforcement Execution): Once the four-month administrative grace period expires, the DWP will actively deploy third-party data tracking and submit formal applications to magistrates’ courts for driving disqualification orders.

Can the DWP Take Money From My Bank Account Directly?

Yes. One of the most significant changes introduced by the PAFER Act 2025 is the removal of the requirement for a civil court order or a formal judgment debt before accessing a debtor’s private financial holdings.

Can the DWP Freeze Your Bank Account Without a Court Order?

The DWP cannot freeze your entire bank account indefinitely, but they can issue an administrative mandate to execute direct deductions, extracting either a single lump sum or recurring deductions from verified financial accounts without a court order.

| Operational Attribute | Previous DWP Boundary | Post-PAFER Act 2025 Framework |

| Court Orders Required? | Yes, required for third-party debt orders. | No, uses direct administrative mandates. |

| PAYE Requirement? | Relied primarily on Direct Earnings Attachments. | Extends to non-PAYE and off-system bank accounts. |

| Pre-Notification | Formal court claim served. | Statutory DWP warning letter (4-month notice). |

| Financial Transparency | Limited to visible asset checks. | Financial institutions must supply limited data verification. |

In practice, this bank account deduction power is tightly bound to the DWP Direct Deduction and Disqualification from Driving Orders Code of Practice.

While the DWP cannot fully freeze an entire account indefinitely to deny a citizen basic subsistence, they can systematically extract identified surplus funds directly from the verified account holder’s balance.

Who is Exempted From a DWP Driving Disqualification Order?

Individuals exempted from a DWP driving disqualification order include those with total debts under £1,000, self-employed tradespeople or couriers relying on their licence for livelihood, designated caregivers, and individuals with severe medical mobility needs.

For active disability benefit recipients, remaining compliant with standard status updates, such as adhering to the PIP claimant’s DWP holiday rules when travelling abroad, is equally vital to prevent administrative issues or accidental overpayment errors.

Essential Needs and Automatic Carer Protections

Carer and medical exemptions automatically protect an individual’s driving licence if the vehicle is proven vital for fulfilling essential caregiving duties for a vulnerable relative or accommodating long-term medical treatments.

The legislation defines specific baseline exemptions where a driving disqualification order is legally impermissible:

- The £1,000 Statutory Threshold: Magistrates’ courts are legally prohibited from granting a driving ban if the total outstanding DWP debt balance sits below £1,000.

- Livelihood Reliance: If an individual requires their driving licence to earn a living, the court cannot issue a disqualification order. This explicitly covers self-employed tradespeople, delivery couriers, and logistics professionals whose employment would instantly terminate without a licence.

- Carer and Dependency Responsibilities: If the vehicle is vital to fulfill essential caring responsibilities for a vulnerable relative, child, or disabled individual, the driver’s licence is protected.

- Medical or Disability Necessity: Individuals who rely heavily on an adapted vehicle due to severe personal mobility challenges or long-term medical treatments are exempt.

How Long Can the DWP Chase a Debt?

The DWP faces no absolute statutory time limitation when recovering benefit overpayments via administrative means. Unlike standard consumer debts, DWP debts do not automatically expire or become unrecoverable after six years.

A common point of confusion among consumers is whether old welfare debts simply expire over time under standard UK debt collection rules.

Can DWP Debts Be Statute-Barred in the UK?

DWP debts cannot be statute-barred under standard UK consumer rules. While the Limitation Act 1980 enforces a six-year limit on private loans, public sector frameworks allow the DWP to administratively reclaim debts that are 10, 15, or 20 years old.

This absolute authority over historical state accounts highlights the long-term reach of public sector finances, mirroring the high-stakes financial scrutiny seen in ongoing state pension corrections like the WASPI DWP compensation January 2026 updates.

Can a Debt Collector Take You to Court After 7 Years for Welfare Overpayments?

A debt collector rarely pursues civil court action after 7 years for welfare overpayments due to policy limits, but the PAFER Act 2025 bypasses county courts entirely by empowering the DWP to collect decades-old debts directly via bank extraction.

What Happens If I Can’t Repay the DWP?

If you cannot repay the DWP, the department is legally obligated to explore affordable repayment options based on an income and expenditure assessment, provided you maintain active communication within the warning window.

How Much Can the DWP Deduct From Benefits If You Are Still a Claimant?

For active claimants, the DWP caps standard recovery deductions between 15% and 25% of the standard Universal Credit personal allowance, depending on whether the debt stems from an administrative error or fraud.

These deductions apply strictly to standard monthly core benefit allocations rather than emergency or historical top-ups, such as the DWP cost-of-living payment 2025 schemes, which were distributed under separate statutory guidelines.

Consider the case of an individual who transitioned out of the benefit system entirely to start a small business. If an old, unresolved Universal Credit overpayment notice of £1,400 is ignored, the DWP may pursue bank extraction or a court-ordered licence review.

However, by engaging with the DWP Debt Management line during the initial warning phase, the individual can safely agree to a nominal monthly repayment plan based on a standard income and expenditure assessment, neutralising further legal escalation.

Summary

The implementation of the PAFER Act 2025 marks a major shift in how public debt is recovered in the UK. While the government aims to protect public funds, the potential for administrative errors means that clear communication is essential.

If you receive an updated DWP debt recovery letter, you should immediately take the following steps:

- Review the paperwork to confirm the exact benefit periods and verify that the overpayment figure matches your historic records.

- Contact DWP Debt Management within the four-month window to discuss an income-matched repayment plan.

- Seek independent guidance from bodies like Citizens Advice, StepChange, or Money Wellness if you face financial hardship or mental health challenges.

FAQ

Is the driving ban automatic?

No. The driving ban is not automatic. It requires the DWP to submit a formal application to a magistrates’ court, proving that the debtor has willfully evaded contact despite having verified financial means to pay.

What is the minimum debt threshold for a driving ban?

Courts can only consider a driving disqualification order if the total outstanding welfare overpayment debt owed to the DWP is at least £1,000.

Can the DWP ban me from driving if I am currently receiving benefits?

No. These specific powers target individuals who have left the welfare system and are avoiding repayment while working outside standard PAYE systems. Active claimants are handled via standard benefit award deductions.

Can a DWP driving ban be overturned or suspended?

Yes. The law stipulates that any driving ban issued under these terms is initially suspended as long as the debtor adheres strictly to the court-approved or DWP-negotiated repayment schedule.

What if the DWP overpayment calculation is an administrative error?

Enforcement can be contested if the underlying debt calculation is incorrect. Data from the DWP Annual Report and Accounts indicates that in the financial year ending 2025, over £540 million was overpaid due to official internal errors, highlighting the necessity of auditing any debt claim before agreeing to terms.