UK-based entrepreneurs often find that securing business credit cards for startups is one of the most significant hurdles when launching a new venture. While traditional lending relies heavily on historical trading performance, modern financial products have evolved to offer more flexible solutions for businesses currently in their early stages of development.

Key Takeaways

- New UK businesses can access credit through specialized corporate cards that prioritize director-level credentials over historical company revenue metrics.

- Most unsecured business credit cards require a personal guarantee from a company director to mitigate the risk posed by limited or no trading history.

- Building a business credit profile requires registering with a UK credit reference agency to ensure accurate reporting of company repayment activities.

- Startups with poor personal credit may find secured credit cards or prepaid expense management platforms more accessible than traditional bank credit.

What is a Business Credit Cards for Startups?

A business credit cards for startups is a revolving credit facility or corporate payment card designed specifically for early-stage companies and new ventures. Unlike standard personal credit cards, these facilities are intended strictly for business-only operational expenses.

They allow a company to manage daily cash flow, cover unexpected outgoings, and equip employees with managed spending power.

Crucially, they serve as a core vehicle for establishing a corporate credit history at UK credit reference agencies, separate from the owner’s individual profile.

Can You Get Business Credit Cards for Startups with No Revenue?

Yes, it is entirely possible to secure a business credit card in the UK even if your venture is pre-revenue or in its earliest developmental phases. The UK fintech ecosystem has dramatically altered traditional lending rules.

Where traditional high-street banks heavily rely on historical tax returns, trading performance, and balance sheets, digital-first lenders evaluate applications based on a composite risk framework.

To qualify without active corporate revenue, lenders shift their focus to:

- Director Credentials: The personal credit record, financial history, and solvency of the resident company director act as the primary risk baseline.

- Personal Guarantees: The majority of unsecured options for new firms require a personal guarantee (PG), meaning the director assumes personal liability for the debt if the business defaults.

- Alternative Substructures: Startups without revenue frequently leverage charge cards (which must be paid in full monthly and don’t carry a rolling interest balance) or secured cards/prepaid expense platforms funded by an upfront deposit.

Best Business Credit Cards for Startups

The UK market features a diverse mix of fintech solutions and traditional banking lines tailored for early-stage companies. The table below compares the leading options available to startups, followed by an in-depth breakdown of each product.

Startup Credit Card Comparison

| Card Name | Annual Fee | Representative APR (Variable) | Primary Rewards | Key Feature / Time Period |

| Capital on Tap (Free) | £0 | 34.96% (Rates from 13.86%) | Uncapped 1% cashback | Up to 42 days interest-free |

| Funding Circle Cashback | £0 | 34.9% (Rates from 14.9%) | 2% intro cashback, 1% flat | Up to 42 days interest-free |

| American Express Business Gold | £0 Year 1 (£195 after) | N/A (Charge Card) | Membership Rewards points | Up to 54 days repayment |

| Barclaycard Select Business | £0 | 25.5% | 1% cashback (on £2k+ spend) | Up to 56 days interest-free |

| Metro Bank Business | £0 | 18.9% | No direct spend rewards | Zero European FX/ATM fees |

| Santander Business Cashback | £30 | 24.3% | Flat 1% cashback | Zero FX fees worldwide |

| Lloyds Bank Business Card | £0 Year 1 (£32 after) | 15.95% | Fuel and EV rewards | Flexible low-rate card |

| Moss Business Credit Card | Custom / Platform fee | 0% (Charge Card) | Up to 0.5% cashback | 30-day payment cycle |

| Capital on Tap Pro | £299 | 34.96% (Rates from 13.86%) | 1% cashback + Avios conversion | Unlimited airport lounge access |

| NatWest Business Credit Card | £0 Year 1 (£30 after) | 24.3% | Merchant partner discounts | Integrated ClearSpend app |

Capital on Tap Business Credit Card

A digital-first unsecured business credit card designed explicitly for growing UK SMEs, requiring a minimal £2,000 monthly turnover threshold and offering instant virtual card deployment.

Capital on Tap is highly favored by early-stage founders due to its soft-search application process and rapid approval engine. It acts as a standard revolving credit facility, scaling up limits as trading volumes grow.

Interest Rate & Credit Limit: Rates from 13.86% to 34.96% variable APR; credit lines available up to £250,000 based on underwriting.

- Pros:

- No annual fee, UK ATM fees, or foreign transaction (FX) charges.

- Uncapped 1% flat cashback redeemable as cash or Avios.

- Cons:

- Requires a minimum established turnover baseline of £2,000 per month.

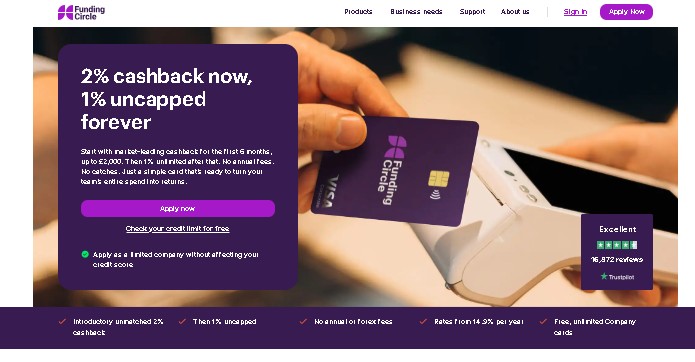

Funding Circle Business Cashback Credit Card

A brilliant option for trimming down everyday business expenses, this card serves up the most competitive introductory cashback rate around for new corporate setups, and there are no ongoing account fees to worry about.

By tapping into its extensive history in SME lending, Funding Circle has built a highly competitive revolving product designed to slash your procurement costs via clear, predictable cash rewards.

Interest Rate & Credit Limit: 34.9% representative variable APR; credit limits range dynamically up to £250,000.

- Pros:

- Generous 2% introductory cashback for the first 6 months (capped at £2,000 total returns).

- Zero annual cost to maintain the primary account or cardholders.

- Cons:

- Requires a minimum established annual revenue of £30,000 to apply.

American Express Business Gold Card

A premier corporate charge card allowing high-spending founders to leverage early operational costs into valuable travel and supply chain reward frameworks.

Because this is a charge card rather than a traditional credit card, it does not carry a standard revolving APR. The balance must be cleared fully every statement cycle, making it ideal for managing immediate, predictable cash flows.

Interest Rate & Credit Limit: No stated APR (charge structure); spending capacity is flexible and dynamically adjusted.

- Pros:

- Up to 54 days of short-term cash flow optimization before repayments are due.

- Robust Membership Rewards point accumulation with a waived first-year fee.

- Cons:

- Strict requirements to pay the complete statement balance in full every single month.

- Substantial £195 annual account fee kicking in from year two onward.

Barclaycard Select Business Cashback Card

If you are a domestically focused startup with lower initial turnover, this high-street option gives you solid institutional backing without any annoying maintenance fees.

Barclays makes things incredibly accessible for early-stage UK firms by keeping the entry revenue threshold exceptionally low, and they even throw in complimentary accounting software integration to sweeten the deal.

Interest Rate & Credit Limit: 25.5% representative variable APR; limits determined individually upon financial screening.

- Pros:

- Extremely accessible qualification criteria requiring only £10,000 in annual turnover.

- Complimentary FreshBooks cloud accounting software integration included.

- Cons:

- High standard non-sterling transaction fees make it poorly suited for international procurement.

- Cashback rewards require a minimum monthly statement spend threshold of £2,000.

Metro Bank Business Credit Card

This is a straightforward, no-nonsense card that pairs one of the lowest standard interest rates on the high street with excellent travel perks across Europe.

It is perfect if you occasionally need to carry a balance from month to month instead of clearing it entirely, keeping your interest costs down without overcomplicating things with messy rewards schemes.

Interest Rate & Credit Limit: 18.9% flat variable APR; conservative, entry-level credit boundaries.

- Pros:

- Highly competitive purchase rate compared to alternative startup lines.

- Completely free cash withdrawals and transactions when operating within European territories.

- Cons:

- Requires the director to hold an active, open Metro Bank business current account.

- Lacks any form of cashback, points, or merchant loyalty incentives.

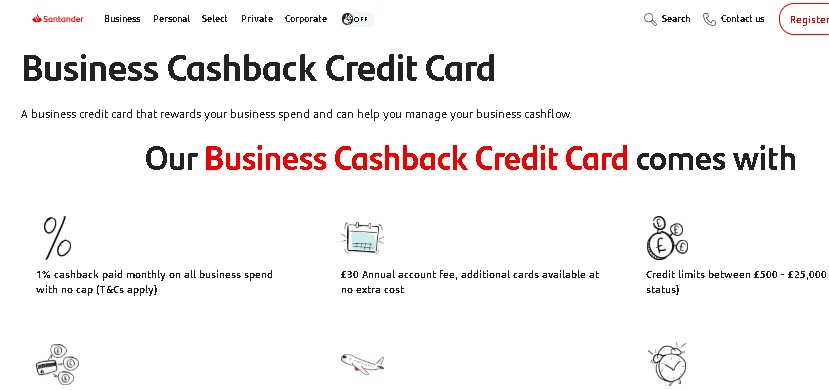

Santander Business Cashback Credit Card

A predictable, flat-rate cashback card built for early-stage companies managing a steady flow of international suppliers and localized business expenses.

Operating with a transparent structure, this card acts as an all-rounder for businesses that require supplementary cards for team members without compounding annual account fees.

Interest Rate & Credit Limit: 24.3% representative variable APR; customized operational limits tailored to bank file depth.

- Pros:

- Uncapped flat 1% cashback returned on all commercial purchases.

- Zero foreign exchange loading fees globally, provided you settle in the local currency.

- Cons:

- Demands a formal, functioning Santander business checking infrastructure to gain approval.

- Carries a fixed, non-waivable £30 annual account fee right from the start.

Lloyds Bank Business Credit Card

A low-interest credit baseline built by a major institution, particularly advantageous for logistics-heavy or mobile startups through structured fuel incentives.

Lloyds focuses heavily on purchase protection and cost reduction across localized travel footprints, combining a competitive core interest rate with a flexible framework for small teams.

Interest Rate & Credit Limit: 15.95% representative variable APR; flexible limit assignments mapped to personal file health.

- Pros:

- Strong cashback and rebate systems tied specifically to national fuel networks and EV charging stations.

- Waived cardholder fee throughout the entire initial 12-month usage period.

- Cons:

- A recurring £32 annual maintenance fee per individual cardholder applies after year one.

Moss Business Credit Card

A heavy-duty, tech-first corporate expense platform built to handle the intense pace of fast-scaling, VC-backed startups.

Rather than acting like a traditional bank, Moss functions as a dynamic operational charge card that aims to eliminate admin headaches through real-time receipt capture and incredibly granular spending controls.

Interest Rate & Credit Limit: 0% interest (strict 30-day corporate charge card structure); high-volume asset-backed capacity.

- Pros:

- Deep real-time oversight features, allowing instant custom spending rules per single card asset.

- AI-driven accounting data parsing that auto-syncs across primary packages like Xero and Sage.

- Cons:

- Inaccessible to micro-entities; targeted strictly at growing finance teams with 25+ staff.

- Carries high software/platform subscription fees instead of traditional lending charges.

Capital on Tap Business Pro Card

A premium-tier corporate reward card built for highly active business directors requiring rapid point generation alongside frequent international business travel amenities.

This upgraded tier from Capital on Tap boosts standard cash returns while providing high-level lifestyle status configurations designed to yield net value to mobile corporate operators.

Interest Rate & Credit Limit: Rates starting at 13.86% up to 34.96% variable APR; access to limits stretching to £250,000.

- Pros:

- Elevated reward points, premium airport lounge access, and Radisson Rewards VIP status benefits.

- 1:1 direct point conversion ratios straight into mainstream travel portfolios like Avios.

- Cons:

- Carries a steep upfront £299 annual cost that must be outpaced by rewards to justify.

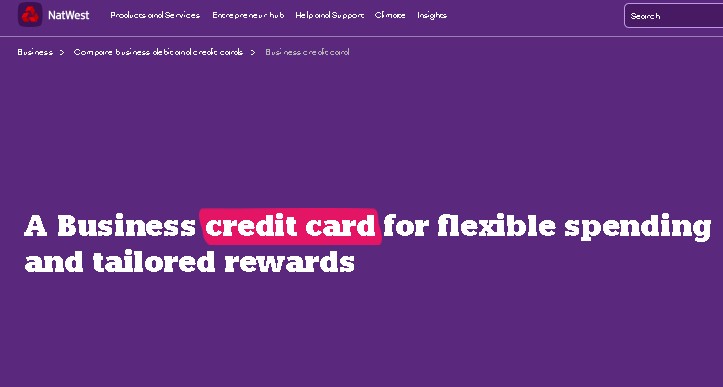

NatWest Business Credit Card

A solid, accessible high-street option offering strong control mechanics via modern applications for firms with early revenue files.

Primarily geared towards existing customers within the NatWest banking loop, this card focuses on ensuring the finance director retains total authority over secondary staff allocations.

Interest Rate & Credit Limit: 24.3% representative variable APR; credit assignments tailored to individual applications.

- Pros:

- Full compatibility with the ClearSpend management app, offering instant, real-time control metrics.

- No baseline card fee levied across the opening 12 months of operations.

- Cons:

- Features a standard £30 per-card annual maintenance fee following the initial year.

- Offers limited direct cashback utility compared to modern fintech alternatives.

What is the Eligibility to Get a Business Credit Cards for Startups?

Lenders use a composite risk assessment framework to evaluate applicants. Because early-stage entities often lack deep commercial credit histories, eligibility is determined by verifying the legal standing of the business alongside the personal financial footprint of the director.

- Legal & Identity Structure: The startup must be registered at Companies House as an active Ltd or LLP. The applicant must be a UK resident director (aged 18+) with a minimum 25% ownership stake, a verifiable UK business address, and an active UK business bank account.

- Credit & Financial Health: Directors must have a clean personal history with no recent bankruptcies, IVAs, or active County Court Judgments (CCJs).

- Revenue Baselines: Requirements vary by card tier:

- Traditional/Unsecured Cards: Often require an established baseline turnover (typically at least £2,000 per month).

- Pre-Revenue FinTech Cards: Underwrite based on equity funding or open banking cash flow projections.

- Secured Platforms: Available to pre-revenue or thin-credit startups via a cash deposit that functions as the credit limit.

- Restricted Industries: Higher-risk sectors, such as cryptocurrency, gambling, weapons, or unregulated real estate, face widespread restriction from mainstream providers.

How to Choose the Best Business Credit Cards for Startups?

Selecting the correct corporate credit tool requires weighing financial terms against your operational habits. Use the following criteria to guide your evaluation:

- Repayment Model: Select a low-APR card if you plan to carry a balance month-to-month. Choose a reward-heavy charge card if you can clear the balance in full every 30 to 50 days.

- Reward Alignment: Pick a card that matches your primary startup expenses, prioritizing high flat-rate cashback for digital ad spend/supplies, or travel points if frequently pitching to investors.

- Software Integration: Ensure the provider features native, real-time Open Banking feeds that link into your core accounting platform (e.g., Xero, QuickBooks, FreeAgent) to simplify expense reconciliation.

- Hidden Fees: Look closely at hidden operating expenses. Avoid non-sterling purchasing costs by choosing a card with 0% foreign transaction (FX) fees if paying international suppliers.

- Credit Impact: Utilize soft-search eligibility checkers first to preserve your credit rating, rather than making multiple direct applications that trigger hard credit inquiries.

How to Prepare Your Application to Increase Approval Chances?

Following a structured approach during the application phase minimizes the risk of rejection. Ensure all documentation is prepared in advance to satisfy the lender’s Know Your Customer (KYC) protocols.

- Gather your Companies House registration number.

- Ensure your business website and social media presence appear active and professional.

- Prepare a clear explanation of your business model and revenue projections.

- Check your personal credit report for inaccuracies before applying.

- Link your business bank account via Open Banking to allow real-time data sharing.

- Compare at least three different providers to find a product that aligns with your specific spending needs.

How to Get a Business Credit Cards for Startups?

Securing a business credit card as a startup requires following a structured approach to satisfy automated underwriting engines and compliance checks. Because early-stage applications heavily weigh the director’s personal file alongside the new entity’s status, skipping steps can lead to immediate rejections.

Follow this execution pipeline to successfully secure your company’s credit facility:

- Build Legal Infrastructure: Legally incorporate as an active Ltd or LLP at Companies House, and establish a dedicated UK business current account matching your company’s exact legal name.

- Audit Personal Credit: Pull your personal credit files to fix errors, clear up address inconsistencies, and ensure you are registered on the electoral roll.

- Gather Required Documentation: Prepare your Companies House registration number, full residential address history for all directors owning $\ge$ 25% equity, and your projected or current turnover figures.

- Use Soft-Search Checkers: Filter card providers using soft-search eligibility tools to check your approval odds and protect your credit score from hard inquiry damage.

- Apply via Open Banking: Submit your application and link your business bank account through Open Banking to give underwriters real-time cash flow verification.

Final Summary

The most effective way to approach startup financing is to align your current business stage with the right product. If you have no revenue, focus on expense management platforms or secured cards to build your initial credit score.

As your company generates cash flow, you can pivot toward unsecured credit lines that offer higher limits and more flexibility.

Disclaimer: The financial rates, fees, and credit parameters outlined in this article reflect current UK market conditions at the time of publication and do not constitute formal legal or financial lending advice.

FAQ

Is it hard to qualify for a business credit card?

Qualification difficulty depends on whether you have existing revenue. For pre-revenue startups, the process is harder and usually requires a personal guarantee. However, fintech providers have streamlined the process significantly compared to traditional banks.

Can I get a business card with no revenue?

Yes, it is possible. Many modern corporate card providers focus on your business’s growth potential and your personal credit history rather than historical trading revenue. These cards often function as charge cards with shorter repayment cycles.

Who is eligible for a small business credit card?

Generally, any registered UK company director with a good personal credit score and a verifiable business address can apply. The business must be legally registered and hold an active business bank account in the UK.

Will applying for a business credit card affect my personal credit score?

Applying for a card usually triggers a hard credit check on the director’s personal file. This may cause a temporary, minor dip in your personal score, but managing the business card responsibly can help build your overall corporate credit profile.

What is a no personal guarantee business credit card?

These are cards that do not require the director to be personally liable for the debt. These are very rare for early-stage startups and are usually reserved for large, established companies with significant annual turnover and asset backing.

Do I need a business bank account to get a credit card?

Yes, you will almost certainly need a dedicated business current account. Lenders use this to verify your business activity, link your financial data through Open Banking, and process your repayments, keeping your professional and personal finances separate.

How do secured credit cards help new businesses?

They allow you to establish a credit history without needing an existing financial track record. By providing a cash deposit, you lower the risk for the lender, which makes them far more likely to approve your application despite a lack of trading history.